15 Smart Ways to Afford Emergency Pet Costs (Even When Money’s Tight)

⚡ Quick Answer

The best ways to afford emergency vet costs are: build a dedicated pet emergency fund, enroll in pet insurance before a crisis hits, use CareCredit or payment plans, and know which nonprofits offer financial assistance. Combining two or three of these strategies gives you the strongest safety net.

📢 Disclosure: This post contains affiliate links. If you make a purchase through these links, we may earn a small commission at no extra cost to you. We only recommend products we believe in.

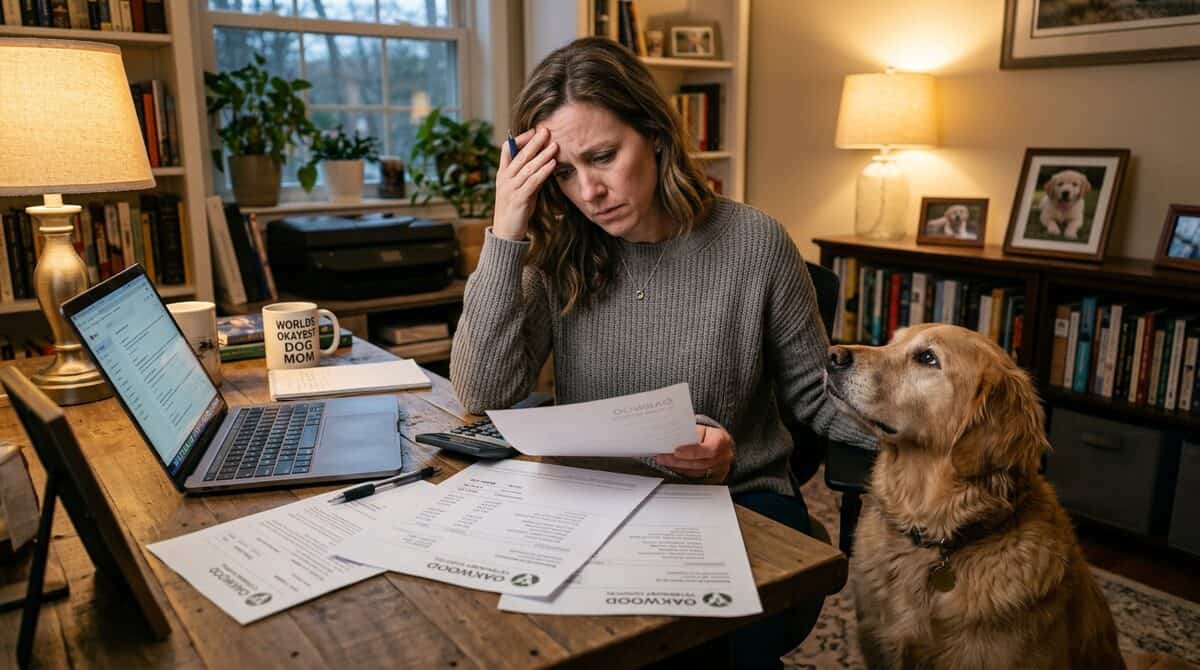

Your dog just swallowed something he shouldn’t have. Your cat is limping and won’t bear weight. The emergency vet bill lands in front of you: $1,200. $2,800. Sometimes more.

If you’ve been there, you know the gut-punch feeling of loving your pet and staring down a number that’s simply not in your budget. It’s one of the most stressful situations a pet owner can face — not just emotionally, but financially.

Here’s the truth: most pet owners are not prepared. A 2023 survey found that nearly 1 in 3 pet owners couldn’t cover a $1,000 emergency without going into debt. And emergency vet visits routinely run $1,500–$5,000+.

The good news? There are 15 concrete strategies you can use right now — from savings systems and insurance to nonprofit grants and negotiation tactics — that can make even the most expensive emergency survivable.

What About Build a Dedicated Pet Emergency Fund?

The single most powerful thing you can do is start a dedicated pet emergency fund before you need one. This isn’t your regular savings account — it’s a separate, untouchable pool earmarked for your pet.

Target: $1,000–$3,000 per pet. Start with a goal of $500 and automate a transfer of $25–$50/month. Keep it in a high-yield savings account so it quietly grows while it waits.

The psychological win of having this fund is real — when an emergency hits, you’re solving a logistics problem, not a financial crisis.

🛒 Pet-Themed Savings Banks on Amazon

What About Get Pet Insurance Before You Need It?

Pet insurance is the closest thing to a financial superpower for pet owners — but only if you enroll before a problem develops. Pre-existing conditions are typically excluded, so the time to act is when your pet is young and healthy.

A comprehensive accident-and-illness plan typically reimburses 70–90% of covered costs after your deductible. Monthly premiums range from $20–$80 depending on breed, age, and coverage level.

Top providers include Trupanion, Healthy Paws, Embrace, and Figo. Compare at least 3 quotes — premiums and reimbursement models vary widely.

What About Use CareCredit or Scratchpay?

CareCredit is a healthcare credit card accepted at thousands of veterinary clinics. It offers promotional 0% interest financing periods (typically 6–24 months depending on the amount charged), which means you can pay the bill over time without accruing interest if you pay it off within the promo window.

Scratchpay is a newer alternative specifically designed for veterinary and medical expenses, with a quick online application and multiple financing tiers. Unlike CareCredit, it doesn’t require a hard credit pull for pre-qualification.

Call your vet’s office in advance to confirm which financing options they accept — not all clinics are enrolled.

What About Ask Your Vet About a Payment Plan?

Many pet owners don’t realize this is an option: you can often ask your vet directly for a payment plan. This is especially true with practices you have an existing relationship with.

Approach the conversation directly and honestly: “I want to get my pet the care she needs — can we work out a payment schedule?” Most practices would rather arrange installments than send a sick animal home or lose a long-term client.

Get any payment arrangement in writing and honor it. Missing payments damages the relationship and may end the arrangement.

What About Look Into Veterinary Schools and Teaching Clinics?

Veterinary teaching hospitals — affiliated with colleges of veterinary medicine — offer specialist-level care at significantly reduced rates. Students perform procedures under close supervision from licensed veterinary professors, often with access to equipment that private practices don’t have.

Costs can be 30–60% lower than private specialty clinics. Find accredited programs through the AVMA directory.

This option works especially well for non-emergency specialist care: orthopedics, oncology, cardiology, and dermatology.

What About Apply for Nonprofit Financial Assistance?

Several charitable organizations exist specifically to help pet owners cover veterinary costs. Eligibility varies, but most consider financial hardship and specific diagnosis types:

- RedRover Relief — grants for pets in urgent situations, especially domestic violence survivors

- The Pet Fund — helps with non-basic, non-emergency care for chronic or serious conditions

- Brown Dog Foundation — focuses on cancer treatment funding for pets

- Frankie’s Friends — specialty and emergency care grants

- The Mosby Foundation — targets pets of low-income owners

Applications take time, so apply early and apply to multiple programs simultaneously.

7. Use the ASPCA’s Resources and Local Humane Societies

The ASPCA maintains resources for pet owners facing financial hardship, including a directory of low-cost vet clinics by zip code. Many local humane societies also operate low-cost wellness clinics or can direct you to community assistance programs.

Don’t overlook breed-specific rescues — they often have emergency fund connections for owners of their target breeds.

What About Start a Crowdfunding Campaign?

In a genuine emergency, crowdfunding can raise money fast. Platforms like GoFundMe and GiveSendGo are free to set up and allow supporters to contribute directly.

Tips for a successful pet crowdfunding campaign:

- Post a clear photo of your pet and a short, honest story

- State the exact amount you need and what it covers

- Share on every social platform and ask friends to reshare

- Update donors with progress — it builds trust and momentum

Pet campaigns often go viral. People love helping animals. Don’t be embarrassed to ask.

9. Negotiate Your Vet Bill (It’s More Common Than You Think)

Vet bills are not always fixed. Here’s what’s often negotiable:

- Bundled services — ask if multiple line items can be combined at a discount

- Hospitalization alternatives — sometimes home monitoring with check-ins is medically acceptable and far cheaper than overnight stays

- Medication sourcing — ask for a written prescription and fill it at a human pharmacy (GoodRx works for many pet meds)

- Staged treatment — some non-urgent treatments can be scheduled over time rather than all at once

The key: be respectful, be honest about your situation, and always ask.

10. Find Low-Cost Veterinary Clinics in Your Area

Beyond teaching hospitals, many communities have nonprofit or sliding-scale veterinary clinics. These exist specifically for financially constrained pet owners.

Search resources:

- Petfinder’s financial assistance listings

- Local Facebook community groups (search “low cost vet [your city]”)

- United Way 211 helpline — often knows local pet assistance programs

- County animal services offices

11. Use Your FSA or HSA (In Limited Situations)

Currently, Flexible Spending Accounts (FSA) and Health Savings Accounts (HSA) do not cover pet expenses under IRS rules — with one notable exception: service animals.

If your pet is a certified service animal (guide dog, psychiatric service dog, etc.), related medical expenses may be FSA/HSA-eligible. Keep documentation and consult a tax advisor.

Some states have begun exploring pet-related tax deductions, so it’s worth checking your local rules annually.

🛒 Service Dog Identification Kits on Amazon

12. Leverage Prescription Savings Programs

Veterinary medications can be marked up significantly at clinic pharmacies. Once you have a written prescription, you have options:

- GoodRx works for many pet medications at human pharmacies (Costco, Walmart, CVS)

- Chewy Pharmacy often beats clinic pricing by 30–50%

- Costco Pharmacy offers deep discounts on generics, no membership required for pharmacy

- 1800PetMeds accepts written prescriptions by fax or mail

🛒 Pet Medication Organizers on Amazon

13. Invest in Preventive Care to Avoid Bigger Bills

The cheapest emergency is the one that never happens. Consistent preventive care catches small problems before they become expensive ones:

- Annual wellness exams catch early disease markers

- Dental cleanings prevent costly extractions and systemic illness

- Flea, tick, and heartworm prevention is far cheaper than treating active infections

- Weight management reduces joint problems, diabetes risk, and heart disease

Some practices offer wellness plan subscriptions (like Banfield’s Optimum Wellness Plans) that bundle preventive care into flat monthly payments — often cheaper than paying per visit.

🛒 Pet First Aid Kits on Amazon

14. Know Your Community Resources Before You Need Them

Community networks can surface help you didn’t know existed:

- Local Facebook pet groups often have pinned lists of low-cost vet resources

- Breed clubs (national and regional) sometimes have emergency funds for their breeds

- Local churches and community organizations occasionally have emergency funds that cover pet care

- Employer EAPs (Employee Assistance Programs) — a small but growing number include pet care financial counseling

Build your resource list now, on a quiet Tuesday, not in the panic of a Friday-night emergency.

15. Consider a Pet-Specific Credit Card or Line of Credit

Beyond CareCredit, some financial products are worth having available before emergencies strike:

- A dedicated low-interest credit card reserved only for pet emergencies — so you always have a known credit line available

- A personal line of credit at your bank or credit union, applied for while your finances are stable

- Scratchpay’s pre-qualification (soft pull only) so you know your approval odds before you’re in a waiting room

The goal isn’t to go into debt casually — it’s to have a pre-approved tool ready so you’re never forced to choose between your pet’s health and your financial survival.