Pet Insurance vs Emergency Fund: 5 Tips

By Jarrod Gravison • Updated April 28, 2026 • 7 min read

⚡ Quick Answer

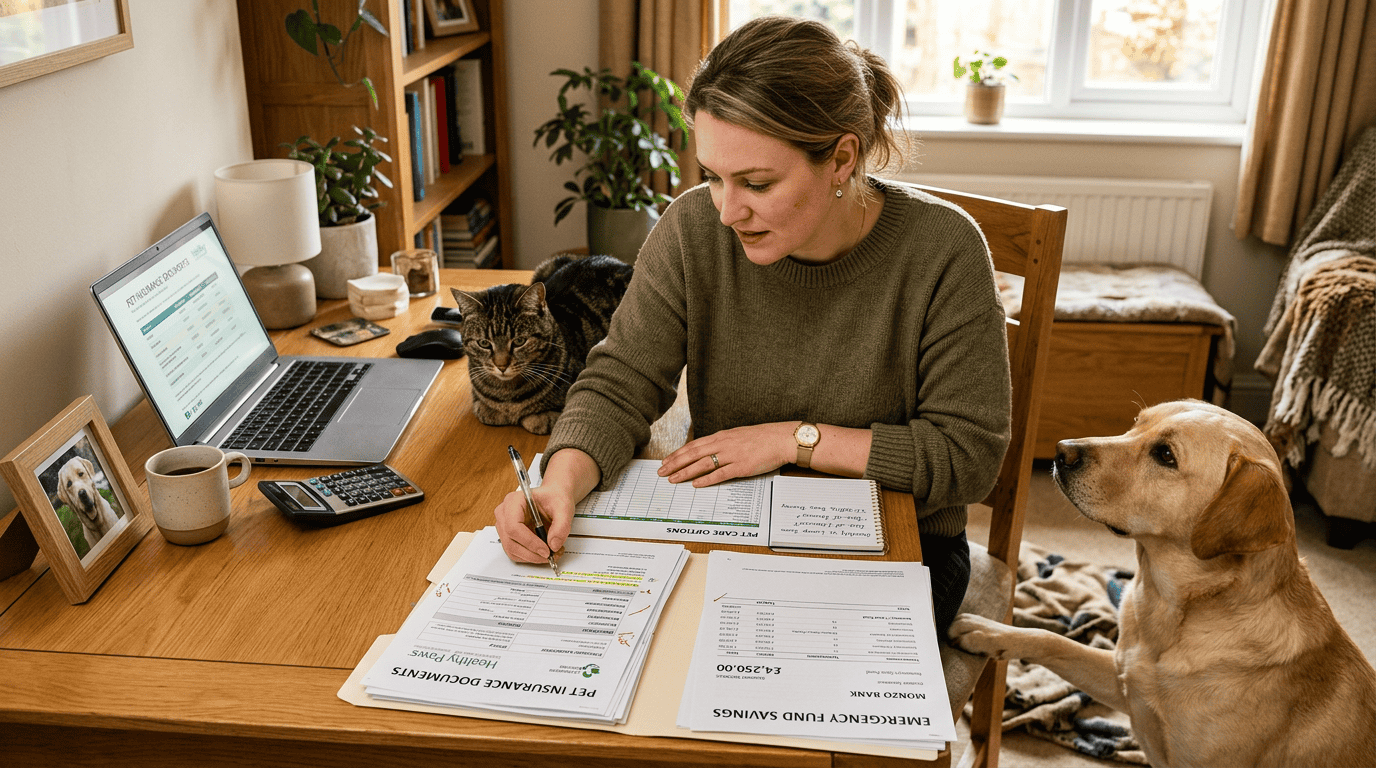

The best approach for most apartment pet owners is both: a $1,000–$2,000 dedicated emergency fund for moderate costs and deductibles, plus pet insurance for catastrophic bills. Insurance without a fund means you need liquid cash for the deductible when you least expect it. A fund without insurance leaves you exposed to $5,000–$10,000+ emergencies.

Disclosure: This post contains affiliate links. We may earn a small commission at no extra cost to you.

Pet insurance and emergency funds serve different purposes and work best together. Here are 5 reasons why the “either/or” framing misses the point.

Key Takeaways

- Insurance and savings work together: The smartest financial strategy combines a $1,000–$2,000 emergency fund for deductibles and smaller bills with pet insurance for catastrophic events — each fills the gaps the other leaves.

- Buy insurance while your pet is young: Pre-existing conditions are excluded from coverage, so a policy purchased at 8 weeks old provides far broader protection than one bought after your pet develops health issues at age 5 or 7.

- Self-insurance requires serious capital: Replacing insurance entirely with savings requires $5,000–$10,000 set aside specifically for your pet — most owners can’t realistically build this before their first major emergency, making early insurance the practical choice.

- Match your deductible to your fund size: If your emergency fund holds $1,000, choose a $500 deductible so you always have buffer left after paying it — this keeps you from being forced to put emergency care on a credit card.

What Should You Know About Reason 1?

Pet insurance is designed for catastrophic, high-cost events — emergency surgery, cancer treatment, serious accidents. These are bills of $3,000–$10,000+ that even comfortable middle-income earners struggle to absorb without notice.

An emergency fund is designed for moderate costs and the costs insurance doesn’t cover: the deductible itself, copays and non-covered services, medication costs below the threshold worth claiming, and small vet visits that don’t meet the claim threshold.

Used together: the fund covers everything up to the deductible + regular non-covered costs; insurance handles everything catastrophic above it.

What Should You Know About Reason 2?

Most pet insurance policies have annual deductibles of $100–$1,000. You pay this amount out-of-pocket before the insurer reimburses anything. If you have a $500 deductible and $0 in savings, you still face a $500 barrier to using your insurance. Without an emergency fund, even insured pet owners can struggle to access care in a crisis.

According to the American Pet Products Association (APPA), the average unexpected veterinary bill ranges from $800 to $1,500 for dogs and $600 to $1,200 for cats — amounts that exceed what most households keep in liquid savings at any given moment. In 2026, emergency veterinary costs have continued rising due to advanced diagnostic technology and specialist care, making insurance deductibles an even more critical consideration.

Practical tip: Keep your emergency fund in a dedicated high-yield savings account separate from your regular savings. This prevents accidental spending and makes it easier to track your actual pet financial cushion. Even $50/month auto-transferred to this account builds a meaningful buffer within a year.

What Should You Know About Reason 3?

Pet insurance becomes exponentially less valuable as pets age and develop pre-existing conditions. A policy purchased at 8 weeks old has no exclusions. A policy purchased at 7 years old may exclude the very conditions most likely to require treatment. If you haven’t bought insurance yet and your pet is:

- Under 2 years: strongly consider insurance

- 2–5 years: evaluate based on breed risk and health history

- 6+ years with conditions: emergency fund is likely more practical

According to the ASPCA, the average annual cost of pet insurance for dogs is $583 and for cats is $342 — but these figures are based on younger, healthier animals. By age 6–8, premiums for many breeds can double as insurers factor in increased risk. This is why the timing of your enrollment decision dramatically affects your long-term cost.

Breed-specific risk is another key factor. The AKC notes that certain breeds — including Bulldogs, Labrador Retrievers, and German Shepherds — are genetically predisposed to expensive conditions like hip dysplasia, heart disease, and cancer. For these breeds, the actuarial case for insurance is especially strong, since a single condition can result in $4,000–$12,000 in lifetime treatment costs.

What Should You Know About Reason 4?

To truly replace insurance with a self-funded approach, you need enough to cover worst-case scenarios: $5,000–$10,000 for catastrophic events like cancer treatment or emergency surgery. Building this takes time. Insurance provides this protection from day one at a manageable monthly cost ($30–$80/month for most pets).

The practical reality: most pet owners don’t build a $10,000 emergency fund for their pet before the first major emergency. Insurance fills this gap.

What Should You Know About Reason 5?

The optimal setup for most apartment pet owners:

- Emergency fund: $1,000–$2,000 in a dedicated savings account. Covers deductibles, copays, smaller emergencies, and moderate vet bills not worth claiming.

- Pet insurance: $30–$80/month. Covers catastrophic bills above the deductible. Match deductible to your fund size — if your fund has $1,000, a $500 deductible leaves buffer.

This approach gives you complete financial protection at a total ongoing cost of $30–$80/month — and eliminates the anxiety of an unexpected $5,000 bill. For detailed insurance guidance, see our 7 tips for choosing pet insurance and pet emergency preparedness guide. The AVMA’s pet insurance guide and NAPHIA (North American Pet Health Insurance Association) are authoritative industry resources.

How Do You Build Your Pet Emergency Fund in 2026?

Even if you have pet insurance, building a parallel emergency fund is one of the best financial moves an apartment pet owner can make. The most effective approach is automation: set up a recurring transfer of $50–$100/month into a dedicated savings account the day you bring your pet home. Over 12 months, you’ll have $600–$1,200 — enough to cover most deductibles and moderate vet bills without touching your main savings.

The ASPCA recommends that pet owners budget at least $200–$400 per year for routine preventive care (vaccines, dental cleanings, annual exams) on top of any emergency reserve. By separating your emergency fund from your routine care budget, you avoid draining your safety net on predictable expenses and are better prepared for the unexpected ones.

For apartment pet owners specifically, consider these fund-building strategies:

- Round-up savings apps: Apps like Acorns or Chime’s round-up feature automatically invest spare change — assign a portion to your pet fund.

- Annual pet care budget: Review your pet’s actual costs each January. If last year came in under budget, transfer the surplus to your emergency fund.

- FSA/HSA alternative: While these don’t cover pets, keeping a separate pet-only savings account functions similarly — earmarked funds you don’t touch for other expenses.

- CareCredit as backup: Not a replacement for savings, but a CareCredit card with a $3,000–$5,000 limit gives you a secondary safety net for emergencies that exceed your fund before insurance reimburses you.

The goal is never to face a situation where financial stress influences a medical decision for your pet. A robust fund + insurance combination makes that outcome much less likely — and gives you the peace of mind to make healthcare decisions based purely on what’s best for your animal.

🛒 Related Picks on Amazon

📬 Free Weekly Apartment Pet Tips

Practical guides for apartment pet owners, delivered weekly.

Frequently Asked Questions

Should you get pet insurance or an emergency fund?

Both: a $1,000–$2,000 emergency fund for moderate costs and deductibles, plus insurance for catastrophic bills. Each covers what the other doesn’t.

When is pet insurance better than a self-funded fund?

When your pet is young (lower premiums, no exclusions), when you have a high-risk breed, when you couldn’t absorb a $5,000+ emergency without hardship, or before you’ve built adequate savings.

When is an emergency fund better than insurance?

When your pet is older with pre-existing conditions that insurance would exclude anyway, when your pet is historically healthy and low-risk, or when your fund has grown to $5,000–$10,000.

How much should you save in a pet emergency fund?

$1,000–$2,000 minimum for moderate emergencies and deductibles. For full self-insurance without coverage, $5,000–$10,000 is the realistic minimum for serious veterinary emergencies.

Can you have both pet insurance and an emergency fund?

Yes — this is the recommended approach. The emergency fund covers the deductible and smaller costs. Insurance covers catastrophic bills that the fund can’t absorb alone.

Jarrod Gravison

Apartment pet specialist at Busy Pet Parent.